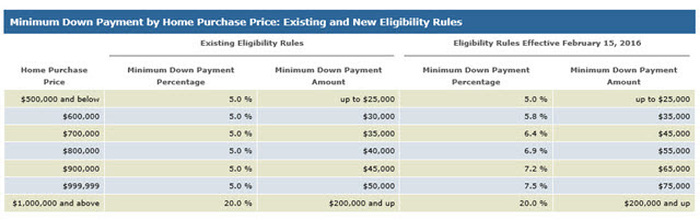

1. So what's really going on? The new policy announced represents a graduated approach to increasing the down payment requirement proportionally to the cost of a home. Canadians who already hold mortgages will not be affected by this announcement. Bill Morneau, the Minister of Finance says "This measure will increase homeowner equity, which plays a key role in maintaining a stable and secure housing market and economy over the long term. It also protects all homeowners, including many middle class Canadians whose greatest investment is in their homes.” 2. What's changing exactly? Effective February 15, 2016, the minimum down payment for new insured mortgages will increase from 5 per cent to 10 per cent for the portion of the house price above $500,000. The 5 per cent minimum down payment for properties up to $500,000 remains unchanged. This change applies to all purchase homeowner loans where the purchase price of the property is greater than $500,000, but less than $1,000,000. 3. How will the new minimum down payment requirement be calculated? As an example, ff you are purchasing a $600,000 home: 5% down on $500,000 = $25,000 + 10% down on the balance of $100,000 = $10,000 for a total minimum down payment of $35,000.00. So to be clear, under the new policy you'll be required to come up with $5000 more for your down payment on the purchase of a home of $600,000.00. A purchase of $700,000 would require the buyer to come -up with $10,000 more for their down payment, etc... How can I plan properly to avoid the increased insurance premium cost? All new insurance applications received on or after February 15, 2016 will be subject to the increase, however, if your application is received before this date you'll save thousands. Its important to note that this does not mean you need to close/take possession of the new home before this date only that your application has to be received. If your application is submitted before February 15, 2016, and as long as the closing date occurs before July 1, 2016 you can still benefit from the lower premiums. C/O Published with Brandon Scott at Benchmark Mortgages. If you have any further questions about mortgages or if you would like your own free consultation with Brandon for a strategy contact Brandon at 780-800-5500 or Brandon@benchmarkab.com  Christian Bailey RE/MAX River City 780-490-6730 |

Archives

June 2020

|

RSS Feed

RSS Feed