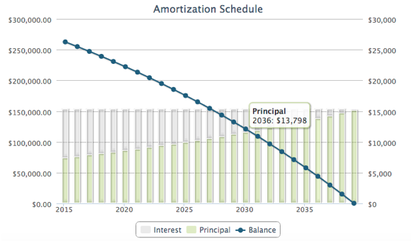

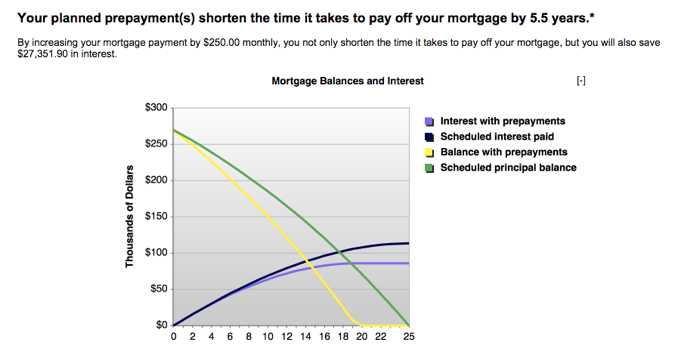

Enjoy Significant Savings with Mortgage Prepayments Many people resort into mortgages to finally pursue the dream of having their own house. Mortgages make this possible, but the only problem is that there are long-term consequences as you have to pay repay it in the future. If you have applied for a 30-year loan, this means that 30 years of your life will be spent paying for the amount you owe the lender. If at any point you would like to shorter the life of the loan, such is possible as you can have issue prepayments. With such, you will be able to shorten the payment period and be mortgage-free sooner than later, which will also be an opportunity for you to invest your money in other channels. How Prepayments Can Help If you are still under a traditional fixed-rate mortgage, you might want to consider prepayment as a way of being able to lower interest. The latter is often the culprit for having to pay more than what you should. The interest rate becomes higher as the repayment period becomes longer. In this case, if you can prepay the mortgage, you will be able to shorten the mortgage term, and hence, interest rate can also be lower. This could possibly cut almost half of the life of the loan in the absence of doubling the payments. With mortgage prepayments, you will also benefit emotionally as you can sleep sound at night knowing there will be nothing to be worried about as you are already done with the payment. Your 30-year loan can be possibly cut into just 15 years if you choose to prepay such. How it can be Done Now that you are convinced on the attractiveness of prepaying your mortgage, the next thing you should do is to get started. You need to consult with your mortgage provider and ask them about the different pre-payment options. In some cases, however, there are penalties imposed but they will be compensated by the amount you will be able to save. Not all lenders will have the same policies, which makes consultation with them necessary as the preliminary step. Nonetheless, before thinking of prepaying mortgage as an option, you have to consider your financial stability. You must be able to have more than enough disposable income or retirement fund to dedicate to the prepayment. If you have other debts, you might want to invest your money in paying them first before it is allotted to prepaying your mortgage. You might also be interested in investing it in retirement accounts. Nonetheless, if the situation is all good, which means you have the resources to dispose, there is no doubt prepaying will be a good choice to accelerate your mortgage. Usually, 80%-90% of your mortgage payment is interest and taxes. Prepayments can be done to ways; 1. Monthly Prepayments. 2. Annual lump sum payment. If your lender will allow both payments, you can cut the cost of you mortgage close to 50%! That means it will cut your 25 year mortgage to 12.5 years by using two methods! Prepaying your mortgage is prepaying the mortgage principal amount without any of your payment going towards the interest. You have to pay it next month anyway, so by paying a portion of your mortgage a head of time, you will cut down the interest on your mortgage and by decreasing your principal. For example, we will assume prepaying our mortgage by $250 each month. Your mortgage of $270,000, amortized over 25 years @ interest rate of 3%(fixed for 25yrs to make it easy). This would usually be payed off by 2040. However, shown in the figure below; you can see how much the savings are only using the monthly prepayment itself. Imagine putting 10%-20% of your payments in a lump sum in addition(only some lenders allow this).   Christian Bailey Licensed Real Estate Professional 902-579-3231 |

Archives

June 2020

|

RSS Feed

RSS Feed